2015: A forgettable year on ZSE

2015 was a forgettable year on the Zimbabwean Stock Exchange (ZSE). Trades have declined drastically, and so too has the exchange’s market capitalisation.

So much has been written on this subject by various analysts but as has been the case in most instances when it comes to national discourse – be it political or business, debates are largely stirred by emotion and good old pragmatism and rationality are thrown away.

Zimbabwe really does have economic challenges and these in turn are affecting several sectors of the economy. Zimbabwe’s capital markets are just but one of those sub-sectors that have borne the brunt of these challenges.

But the temptation to look at Zimbabwe or its equities market in isolation and lament as atrocious, execrable or pathetic (take your pick), the ZSE’s performance, must be avoided, regardless of how easy that would be to do.

The global economic landscape has been tough, particularly for most emerging markets, this year. Despite a wave of optimism attached to developing nations, especially coming out of the Global Financial Crisis, most of these economies look like big-time losers now following periods of lean returns.

Granted in the grand scheme of things, Zimbabwe is somewhat semi-detached from the global economy, and the huge outflow of funds from most emerging markets in Africa that has been witnessed recently, does not affect Zimbabwe given the fact that inward flows of global funds onto our “shores” are largely non-existent.

Year-to-date (Y-T-D), data shows that most bourses recorded negative returns as at November 30 in US dollar terms. For instance the Botswana Stock Exchange recorded -2.4 percent; the Lusaka Stock Exchange achieved -45.6 percent and the Nairobi Securities Exchange had -21.9 percent.

Even the continental heavyweight bourses such as Nigeria and Ghana had -27.1 percent and -26 percent respectively. In fact, of the exchanges we track, only the Namibian exchange and the BRVM – a unique regional bourse for the eight countries in of the West African Economic and Monetary Union recorded positive returns. What is the implication of all this to the Africa focused investor?

The stock market is under pressure and company earnings are depressed, mirroring the global economic outlook. There is an obvious need to look to a different asset class, to maintain positive returns, in view of the stock market’s heady days coming to a break. Both local and international investors would do well to look to private equity.

According to the latest Search for Returns survey, 80 percent of the investors who participated expect the African private equity market to outperform African listed equities over the coming decade.

In the search for returns, this asset class has the potential to reward investors handsomely, and as more Africa focused private equity funds scour across the continent, Zimbabwe should prime itself to benefit from this increased focus on private equity by global investors.

Private equity is largely underrepresented in Africa yet it brims with potential to deliver superior returns as large and more developed bourses are maturing and delivering weaker returns.

This provides scope for even those investors who have been evading investing in Zimbabwe’s capital markets to tap into this sector for higher investment returns.

But regulatory authorities and policy makers also need to focus on transforming Zimbabwe’s market conditions to make them more appealing for private equity investors.

The private-equity industry needs policies and regulatory frameworks that foster its growth. Most private-equity funds on the continent are registered in countries with good regulations, and flexibility in the free flow of funds, and this would be the unnegotiable expectation for investment destinations like Zimbabwe.

Furthermore, viable exit options in the market must be made available to investors to enable them to realise value once they have invested locally. Normally pension funds are restricted in what they can invest in for reasons of prudence, including even restrictions in investing in companies that are listed on stock markets in certain cases.

Reforms must be made such that, pension funds are invested in private equity, albeit wisely and responsibly.

The bottom-line is that, the stock market has become what we have been traditionally accustomed to. But as equities continue to be pummeled, return-starved investors can look to private equity and allocate more capital to this asset class.

Benefits to be derived from private equity are multi-pronged ranging from alternate sources of funding for businesses in the country, to funding capital rich projects such as power generation and infrastructure development.

This means that benefits can accrue to both private investors and the nation at large, if private equity is allowed to gain more traction. – Wires

You Might Also Like

-

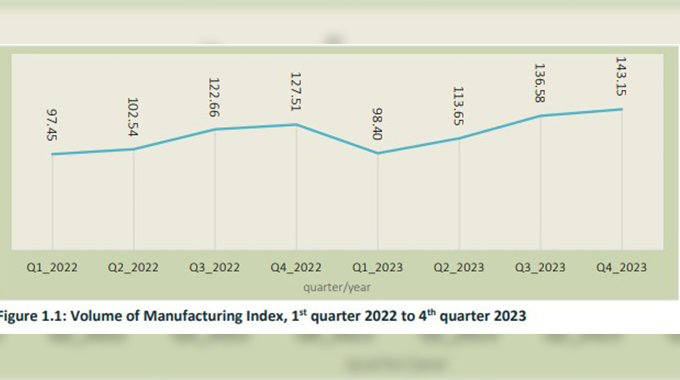

Sikhulekelani Moyo ZimStats says the manufacturing index for the 2023 fourth quarter registered a 12,26 year on year percentage increase to 143,15 when compared compared to 127,51 recorded in the prior year. Volume of the manufacturing index (VMI) is an economic indicator that shows relative changes in the volume of output in the manufacturing sector over time, […]

Agriculture Journal

Comments