Cash shortages an opportunity for innovation among cross border traders: Cash shortage Q and A

Clients stand outside a Bulawayo bank for their chance to do transactions in this file picture. Zimbabwe is facing severe cash shortages that have resulted in long queues at banking halls, and this has negatively affected both the formal and informal sectors

Francis Mukora

ZIMBABWE is facing severe cash shortages that have resulted in long queues at banking halls, and have negatively affected both the formal and informal sectors.

Business Chronicle correspondent Francis Mukora (FM) sat down with Zimbabwe Cross-Border Traders’ Association (ZCBTA) secretary-general Augustine Tawanda (AT), in a bid to understand how the cash shortages have affected informal cross border traders in Bulawayo.

Below are excerpts of the interview.

FM: In your opinion, what have been the major causes of the acute cash shortages that Zimbabwe has been facing for close to a year now?

AT: One of the reasons why there have been these cash shortages is, in my view, the decreasing levels of public confidence in the banking sector.

You will recall that when we had a crash of the Zimbabwean dollar around 2008, people lost confidence in the banks. Now we were just beginning to gain confidence again, and something happened, then people began scrambling for their cash, or whatever was in the bank.

FM: What is the something that happened and caused people to scramble for cash?

AT: Basically, it was the introduction of the bond notes. People thought we were going back to the 2008 situation, and this triggered old memories and dented the confidence that they were now beginning to have in the system. People started to take precautionary measures, such as panic withdrawals. So, to a larger extent, much of the demand for cash was not really for transacting, but hedging for security reasons. It was more like moving their money from the banks to the mattresses, and this is what caused these acute cash shortages.

FM: To what extent, and in what major ways, have you, as cross border traders, been affected by these cash shortages?

AT: Like anybody else, accessing cash has been a challenge which impact negatively on transactions, whether you want to pay school fees or purchase stocks for replenishing your business supplies. But I think the effect of the cash crisis on cross border and other informal traders may not be as severe as it is on the manufacturer who has to apply for foreign currency from the Reserve Bank of Zimbabwe. One thing that you should also be looking at as you interrogate the cash shortages is that it is actually the formal system, which might be failing to lay its hands on foreign currency and not necessarily the ordinary people. I will give you an example of the long queues that you saw at the banks as parents were paying school fees when schools opened. This is the money that was under the mattresses, but it is only coming into the formal system at this particular point for a particular purpose.

As for cross-border traders, they would only be affected by the cash shortages in the context of getting payments for goods sold and services rendered. If you take it from the perspective that generally the cash shortages were caused more by mattress banking, it then implies that traders actually have the money to transact but the challenge would be how to get the money from their clients after selling the wares. To me, that would be the starting point in examining the challenges faced by cross border traders due to the cash shortages.

FM: Late last year, Government introduced bond notes to ease the acute cash shortages. Did the introduction of bond notes improve business among your members?

AT: Definitely. The introduction of bond notes ameliorated the liquidity situation and now, the more the bond notes come in, the less the queues you see at the banks, and the more you see money circulating around. So yes, in a way, the bond notes improved business, not only among cross border traders, but for all other sectors as well. But to me, it was more about the way the bond note was introduced. I think the Reserve Bank managed the process very well in that it maintained confidence in the currency, thus gradually releasing the pressure and gaining public trust in the currency.

This is what made the bond note a success.

FM: Still on the issue of bond notes, the RBZ said they were also introduced as an export incentive for exporters generating foreign currency. What measures have your association and its members taken to benefit from the export incentive aspect of the bond notes?

AT: As enunciated by the Reserve Bank, there are no specific benefits for the cross border traders per-se, as it mainly targeted big players in the formal sector. However, there are policy intervention opportunities and a chance for us as cross-border traders to help industry to recover. We should really start looking at cross-border trading as a special zone and an opportunity for turning the bond note into some kind of foreign currency. We feel, as small scale players, that the Reserve Bank can actually help to boost exports by also promoting productivity and facilitating capacity utilisation at the micro level. What I am saying is that, we can go back to the situation before 2008 when cross border traders were net exporters who were not worried about foreign currency. They would take their curios to South Africa and bring back the rand. But when we dollarised, we actually changed from being an export driven enterprise, to an import driven enterprise whereby after selling their wares outside the country, cross-border traders would then bring in other wares to sell and make the US dollar. But with the introduction of bond notes as an export incentive, we now need policy innovation from the Reserve Bank. We have been engaging the Reserve Bank to see how cross border traders can access the bond notes export incentive. So we have already presented papers to Government and the Reserve Bank of Zimbabwe with various proposals on how this can be achieved.

FM: What are some of the proposals you have made and how has Government responded?

AT: We lobbied the Ministry of Finance, the RBZ and the Ministry of Small to Medium Enterprises for financing of the cross border trading sector and reforming the trading environment. We actually advised Government that, look, you can be able to harvest from the energy of the cross border traders if you put aside funding for our operations. We said to them, as cross border traders we are prepared to burn the midnight candle to export and bring in both foreign currency and raw materials that will drive productivity in our industries. We also proposed the creation of a float, in bond notes, for cross border traders and artists who buy things such as art and craftwork from the curio manufactures to be able to buy them in bond notes, take them for sale outside the country and be able to deposit whatever foreign currency they get there into an account and then be able to come and withdraw it here as bond notes. This way, we would be converting the bond note into foreign currency. Since 2004, we have also, as ZCBTA, advocated for what is called COMESA Simplified Trade Regime (STR), whereby we lobbied that people must be allowed to import or export goods of up to $1000. without a lot of paperwork requirements such as invoices or Bills of Entry.

In 2010, COMESA acknowledged that and they introduced STR, but our Government was not innovative enough to create policies, which would enable us to capitalise. For instance, instead of using the STR as a mechanism to tap into the foreign currency generation capacity of the informal sector, Government opened it up to everybody.

However, we are now happy that they have responded to our proposals particularly through the $15 million loan facility that was availed specifically for cross border traders.

FM: Tell us more about the loan facility. Who will benefit and how will it work?

AT: Like I said earlier on, the $15 million Fund is an outcome of the engagements with Government. In fact, four years ago we had approached Afreximbank with the same proposals we made to the Zimbabwean Government and they saw the value of bringing the micro enterprise player into the formal economy. They actually put significant funding on the table but we could not find a banking partner with expertise to manage the finances in accordance with their expectations and the deal could not proceed. But now we are happy that our own Government has come on board.

The purpose of the funding is two-pronged. Firstly, it is export focused and secondly, it is production focused. You must have something to sell outside the country or you should be able to bring in raw materials which add value to the country’s productivity for you to be able to access this funding. You cannot borrow that money to import finished products. We have established a partnership with Steward Bank who will be the fund manager. We will soon be meeting the RBZ to finalise the operational parameters before we roll out the facility but I can give you the background information. The loan facility will only be accessed by cross border traders who belong to organised structures. In terms of eligibility requirements, we as ZCBTA are proposing a shift from the geography related rules used by micro-finance institutions. For us, there is no point in asking somebody about a fixed place from which they operate because a cross border trader can be working from home but trading around the country. So what we should be looking at is the track-record.

To say that, if you have been exporting wood can we see your forestry papers or proof of the duty that you have been paying say for the past three years. Secondly, we will also encourage our members to organise themselves and apply as small groups as a way of minimising default risks. Lastly the Government has also said we do not want this facility to benefit people from Harare only and so as we speak, we have triggered registration in all other provinces to get a decentralised membership database. Generally, we see it as a win-win situation and a strategic alliance between Government, CZI and us the cross border traders. For us cross border traders, it’s about increasing capitalisation and viability, for the Government it’s about earning foreign currency and for CZI they can follow our footprints a few years later to open bigger shops.

FM: Cross border traders require foreign currency to import. How accessible has it been especially now that the bond notes seem to be replacing the US dollar in circulation?

AT: Well, I haven’t heard people cry because right now, getting foreign currency in the bank or outside the bank is not necessarily an issue in this country. Remember I talked about the issue of mattress and for instance if you give an order to an informal trader for a specific product today, they will simply get their foreign currency from under the mattress and go and import the product for you. What Government needs to do, which we have proposed to them, is to create incentives for people to bring out the money from under their mattresses and transact. One such measure is to allow informal traders to import strategic raw materials and also lower duty on those raw materials, which are key for revival of our industry. Those who cannot get foreign currency from the banks have their own networks of accessing it on the parallel market.

FM: But isn’t there a challenge with the exchange rates, because while the RBZ says the bond note is at par with the US dollar, there have reports that this isn’t the case on the parallel market.

AT: I really haven’t heard many of such stories because people are using bond notes and the US dollar at the same time and these currencies are being treated at par. What I have heard, but I haven’t been able to prove it, is that when the bond note was introduced, there were shops that were insisting on payments in strictly US dollars and not bond notes. But if you talk about roadside moneychangers, I haven’t heard any complaints and so like I said exchange rates have not really been a problem for cross-border traders. In fact informal traders can actually do their business without even going to the banks.

FM: What innovations have you taken as an informal business sector to ensure that your membership’s business is not severely affected by the decrease in cash circulation levels?

AT: The innovation that we did as cross border traders has been to develop a new membership card which also functions as a bank card and it is powered by Steward Bank. This is part of a move towards a cashless society within the cross border traders sector which also helps to minimise the negative impact of cash shortages on our membership. You can tell the people in Bulawayo that as an association, we have developed a branded bank card, which enables our members to transact locally without necessarily having to use cash all the time. We partnered with the Confederation of Zimbabwean Industries and Steward Bank, so that we have that kind of a technical transacting platform. But this card is ZimSwitch enabled and only works locally. I can safely tell you that within another three weeks, we will have a cross border card, which operates beyond our borders. We are just putting the nuts and bolts together.

Secondly, this transacting platform, which will help the small-scale cross border traders to talk to big traders in terms of business. In other words, I can walk into Dairibord or Olivine Industries, swipe using this card and get a discount. We also have Point Of Sale machines which you can use to make purchases using this card. The key feature, which I want you to capture is that we requested for specifications, which allow inter-member payments using this card. In other words, if a cross border trader in Victoria Falls wants bananas which I can send from Harare, we should be able to pay each other using the plastic card.

FM: How has the membership responded to this card and what has been the uptake level?

AT: So far the card has been doing well in Harare. Right now we are putting the mechanisms in all provinces to enable people to access it and also register as members. Since the announcement of the loan fund, the demand for the card has been rising significantly. Initially we had said we will start doing the campaigns in Harare and learn how to replicate it in the provinces.

FM: How would you compare the impact of cash shortages to that of Statutory Instrument 64 of 2016?

AT: Statutory Instrument 64 had both positive and negative impacts on our operations as cross-border traders. The negative impact mainly relates to the way it was introduced. It was introduced at a time when cross-border traders were already strangled by another instrument, called Instrument 148, which had been introduced much earlier.

It prevented traders and travellers using buses with trailers from enjoying tax rebate. So Statutory Instrument 64 was introduced when cross border traders were already under siege and tempers were boiling. They were saying- How can you have someone driving a Mercedes Benz being allowed a $200 rebate but a poor person using a bus with a trailer is not allowed?.

But suffice to say that the Ministry of Industry and Commerce was very proactive in dealing with the situation and we were called to a meeting where we then began to input in the process, which had been started without involving us. We made our submissions, which were taken on board. We pointed to the minister that apart from being a livelihood for many people, cross border trading can also support the recovery of the economy. We said for whatever import gap there is in this country, there must be some kind of framework, which allows a small-scale trader to also play a part.

We suggested to them to give us a list of goods or raw materials that can be imported so that we can incentivise people with money under their mattresses to bring it out, engage in business and ease the cash shortages.

The minister was very accommodative and I can speak with authority that if any of our members require import permits, all we need to do is to write a support letter to the minister and they will be able to get it and import whatever is being imported by the big players.

FM: What would be your closing remarks; any advice or the way for your members and Zimbabweans at large?

AT: I would like to urge our members out there to register for them to enjoy the many benefits that our association has to offer, such as the impending loan facility and the cross border traders’ card that will enable them to boost their businesses in these times of cash shortages and also to get discounts from manufacturers.

You Might Also Like

-

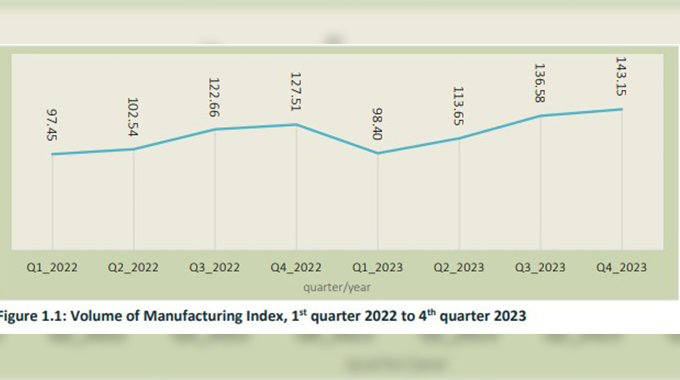

Sikhulekelani Moyo ZimStats says the manufacturing index for the 2023 fourth quarter registered a 12,26 year on year percentage increase to 143,15 when compared compared to 127,51 recorded in the prior year. Volume of the manufacturing index (VMI) is an economic indicator that shows relative changes in the volume of output in the manufacturing sector over time, […]

Agriculture Journal

Comments