Microfinance institutions urged to comply with laws

Dr Charity Dhliwayo

Oliver Kazunga Acting Business Editor

THE Reserve Bank of Zimbabwe (RBZ) has issued a circular to money lending and microfinance institutions urging them to comply with the minimum capitalisation levels announced in the 2014 monetary policy statement.Deposit-taking microfinance institutions are required at present to operate with a minimum capitalisation of $5 million and $10 million by December 31, 2020.

Credit-only microfinance institutions (including money-lending institutions) are required at present to maintain minimum thresholds of $20,000 and $50,000 by December 2020. “Microfinance institutions are expected to take note and take the necessary steps to ensure compliance with the above-stated minimum capital requirements,” said the central bank in a circular dated February 18, 2014.

Meanwhile, in the 2014 monetary policy statement last month, RBZ acting Governor Dr Charity Dhliwayo said microfinance the world over plays a pivotal role in promoting financial inclusion through availing credit, facilitating employment creation and providing access to finance to marginalised communities.

She said it was therefore important to ensure microfinance institutions had sound financial base. She, however, said the RBZ noted that microfinance operations in Zimbabwe were presently skewed towards consumptive lending at the expense of productive sector financing, thus crowding out small and medium enterprises.

“The high level of consumptive lending has also precipitated household over-indebtedness. In view of this development, we encourage microfinance institutions to reorient their lending portfolios and ensure that their lending is directed more towards the productive sectors of the economy,” she said.

Dr Dhliwayo added that the promotion of SMEs and community development was critical taking cognisance of the new realities where they account for significant economic activity.

She encouraged financial institutions and other stakeholders to increase their support to the SMEs sector. “Smallholder farmers continue to be deprived of much needed agricultural funding as a result of constraints mainly related to lack of collateral. Further, most small-holder farmers lack agricultural expertise.

“The de-industrialisation of the economy has given rise to the influx of SMEs in the manufacturing sector which require financial and technical support. The same holds for other SMEs in the various sectors of the economy.

“We urge development partners and financial institutions to facilitate the provision of appropriate and affordable credit to SMEs through the establishment of soft funding schemes. The schemes should incorporate a capacity building component,” she said.

You Might Also Like

-

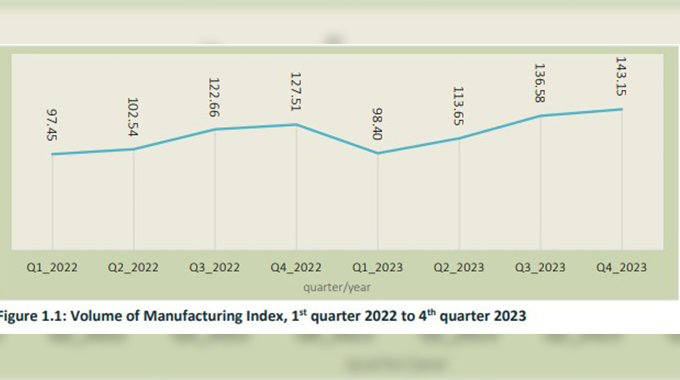

Sikhulekelani Moyo ZimStats says the manufacturing index for the 2023 fourth quarter registered a 12,26 year on year percentage increase to 143,15 when compared compared to 127,51 recorded in the prior year. Volume of the manufacturing index (VMI) is an economic indicator that shows relative changes in the volume of output in the manufacturing sector over time, […]

Agriculture Journal

Comments