MTP to revamp capital markets

Medium Term Plan.

The MTP will ensure implementation of the revised Reserve Bank Act by 2011 and vibrant money and capital markets during its five-year tenure.

Presently, the Zimbabwe Stock Exchange is the most active and reasonably rewarding capital market. The money market has been operating in fits and starts, as there are no attractive returns on placements.

The MTP also targets enhanced financial sector supervision and surveillance, growth of small to medium enterprises, macro-finance banking, a secondary bourse for SMEs and properly priced risk weighted financial instruments.

Objectives of the new policy include greater mobilisation of financial services to productive sectors through more financial intermediation, increased access to financial services and low, competitive interest rates.

But main challenges facing the sector include low liquidity, lack of long-term funding, interest rate and limited range of money market securities.

Government, through the MTP, will strive to adopt policies that seek macro-economic stability, foster market determined interest rates and implementation of the revised RBZ Act to enforce prudent banking practice.

Analysts said the local banking industry was seriously disfigured largely as a result of the liquidity constraints pervading the entire domestic economy.

This has seen several banks taking advantage to charge uneconomic interest rates that have discouraged local firms from borrowing to fund operations.

Liquidity constraints have also created headaches for indigenous banks with less financial muscle, which has resulted in the death of the interbank market and this has negatively impacted financial intermediation.

Zimbabwe requires about US$8 billion for economic reconstruction and due to a decade of economic instability there is little internal liquidity to support growth and development of money and capital markets.

Government has targeted revamping financial markets on the realisation of the role of the financial sector in mobilising funding for productive sectors.

Financial intermediation has improved gradually following the adoption of the multi-currency in 2009 and a number of economic recovery measures.

As at June 2011 there were 27 banking institutions, 16 licensed asset managers and 114 operational macro-finance institutions supervised by the Reserve Bank.

Since adoption of the multi-currency system bank deposits have risen from US$298 million in January 2009 to US$2,6 billion as of December last year.

During this period a total of US$1,3 billion was extended to industry, translating into a loan to deposit ratio of 65 percent, but short-term deposits during this period accounted for 93 percent of total bank deposits.

Through the MTP, Government also envisages creating an efficient national payment system, Central Securities Depository and automated trading system.

“The national payment system, which was resuscitated in March 2009, is gradually being modernised and diversified through banks and other stakeholders.

“The Zimbabwe Stock Exchange, which plays an integral part in mobilising investment resources, has also improved its performance since the introduction of the multicurrency system,” reads an excerpt of the MTP.

l This is the eighth part in a series of articles on the key deliverables of the Medium Term Plan crafted to guide Government programmes in the period 2011-2015.

You Might Also Like

-

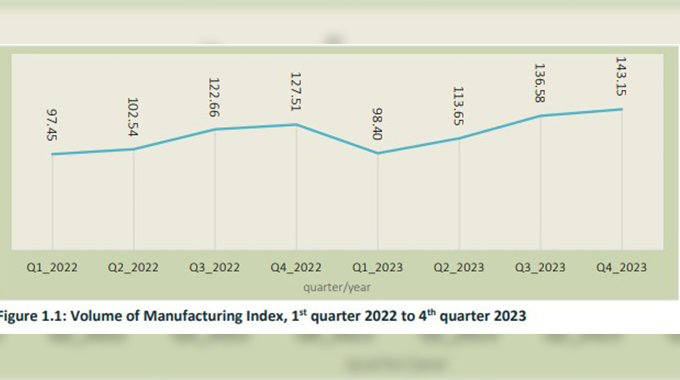

Sikhulekelani Moyo ZimStats says the manufacturing index for the 2023 fourth quarter registered a 12,26 year on year percentage increase to 143,15 when compared compared to 127,51 recorded in the prior year. Volume of the manufacturing index (VMI) is an economic indicator that shows relative changes in the volume of output in the manufacturing sector over time, […]

Agriculture Journal

Comments