RBZ drafts consumer protection document

Bianca Mlilo, Business Reporter

THE Reserve Bank of Zimbabwe (RBZ) has come up with a consumer protection prudential standards document, which lays down guidelines on best practises for banks.

The document, which was seen by Business Chronicle, is being circulated among stakeholders for input before finalisation at the end of July 2016.

In it, the central bank’s supervision directorate headed by Mr Norman Mataruka orders banks in Zimbabwe to implement policies of disclosure from the time a client opens an account with a bank.The guidelines are meant to safeguard the public from being ripped off.

“Upon opening a new account for a person, banking institutions should disclose interest rates, fees and charges to their customers,” reads part of the document.

“A banking institution will be required to provide the person in writing with a written statement of all its charges for maintaining the account and allowing the person access to the funds in the account, the interest it will pay on the funds in the account, and the interest the person will have to pay on any overdraft.”

The RBZ said regulated entities (banks) and their authorised agents should set out and explain clearly the key features, risks and terms of the products, fees, commissions or charges applicable.

It further notes that where a banking institution extends credit to a borrower, it is supposed to disclose to the borrower in writing the interest charged and the manner in which it was to be calculated.

Banks are also required to assume responsibility for the disclosure of any fee or charge, terms or conditions applicable to the credit and identify the obligations of the borrower.

“When a regulated entity realises collateral on a debt, it shall remit to the customer surplus after settling the debt and shall not levy exorbitant charges,” said RBZ.

It said the objectives of these prudential standards were to increase public awareness of financial services and products, promote greater transparency and minimise information asymmetry between consumers and regulated entities hence ensuring that consumers are enabled to make informed decisions.

The guidelines are also meant to ensure availability of consumer redress and development of formal or informal robust grievance redress mechanisms.

You Might Also Like

-

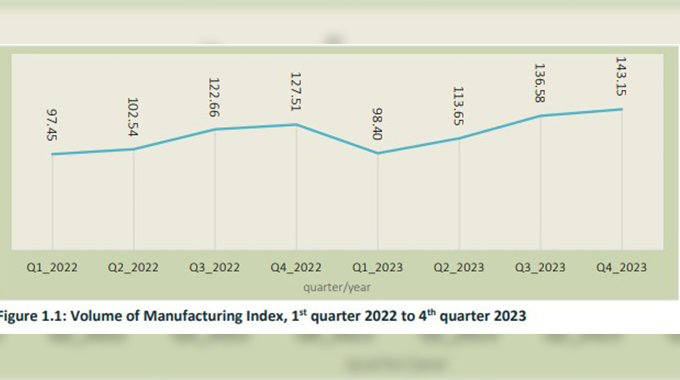

Sikhulekelani Moyo ZimStats says the manufacturing index for the 2023 fourth quarter registered a 12,26 year on year percentage increase to 143,15 when compared compared to 127,51 recorded in the prior year. Volume of the manufacturing index (VMI) is an economic indicator that shows relative changes in the volume of output in the manufacturing sector over time, […]

Agriculture Journal

Comments