State, Essar Africa to seal Zisco deal

By Golden Sibanda

Government and Essar Africa are expected to conclude the Ziscosteel deal this week, amid reports that the partners are putting last-minute fine-tuning, largely on the debt issue.

This follows two weeks of intense talks on the Zisco debt, estimated at US$240 million.

Industry and Commerce Minister Welshman Ncube yesterday told Herald Business that the parties were still on the ground, trying to agree on certain legal aspects of the contract.

“People are still on the ground trying to change this and that law in the (contract) document, but we must have a full document by the end of this week,” said Minister Ncube.

Government announced in November last year that it had settled for Essar Africa as the preferred investor for its 54 percent shareholding in the cash-strapped steel giant.

Deputy Minister of Industry and Commerce Mike Bimha had said then that they expected Essar Africa to be on the ground before the end of the year, which Essar fulfilled.

But despite moving on to the site, the parties were yet to sign an agreement to make the deal fully binding.

It emerged last month that the parties held several meetings to find common ground on a US$28 million foreign debt owed by TelOne, which threatened to scuttle the deal.

TelOne owed Dutch Bank ING US$28 million from a loan facility advanced in the 1980s.

Government had guaranteed the transaction, which had now sucked in Essar Africa.

ING Bank were now demanding that Essar pay off the debt from the funds due to Government from the sale of the Ziscosteel stake. But Government would not hear of it.

Minister Ncube said the challenge regarding the TelOne debt had now been resolved.

The complications had threatened one of the most promising opportunities for the revival of Ziscosteel, which stopped production half a decade ago due, largely, to a financial crisis.

Similar efforts to resuscitate the firm failed in 2004 when a US$400 million deal with Global Steel Holdings of India collapsed under unclear circumstances when the firm pulled out on the 11th hour.

As part of its desire to revive the Redcliff- based former steel giant, Essar committed to pay off the Ziscosteel’s US$240 million debt to Germany’s KFW Bank and an unnamed creditor from China.

Apart from settling the debt, Essar will pay US$55 million for the shareholding and about US$65 million on reviving blast furnaces and coke oven batteries.

Ziscosteel was a vital, strategic asset for Zimbabwe and Essar has pledged to use the firm to develop the economy.

Essar outwitted steel-making giants such as Jindhal Steel and Power of India, Arcelor Mittal of South Africa, Murray & Roberts and Reclamation (SA), Steel Makers Zimbabwe, the Gateway Consortium — a consortium of local and SA investors — in clinching the deal.

You Might Also Like

-

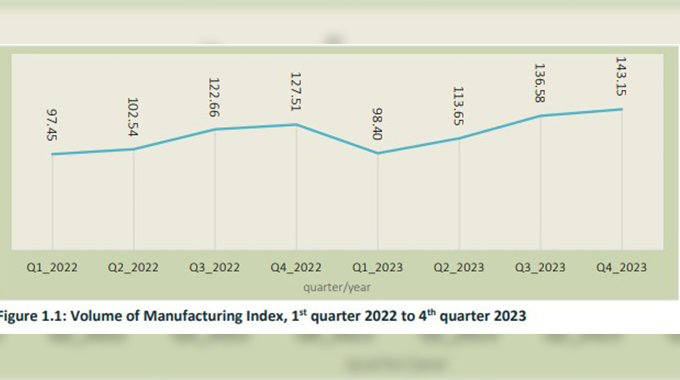

Sikhulekelani Moyo ZimStats says the manufacturing index for the 2023 fourth quarter registered a 12,26 year on year percentage increase to 143,15 when compared compared to 127,51 recorded in the prior year. Volume of the manufacturing index (VMI) is an economic indicator that shows relative changes in the volume of output in the manufacturing sector over time, […]

Agriculture Journal

Comments