Using intellectual property assets for SMEs financing

Aleck Ncube

THERE has been a growing awareness that intellectual property (IP) assets can be monetised. There are various ways to do so. IP can be sold, licensed, used as collateral or security for debt finance, or it can provide an additional or alternative basis for seeking equity from friends, family, private investors (the so-called “business angels” who invest in unquoted small and medium-sized enterprises (SMEs) and often also provide experience and business skills), venture capitalists, micro-finance institutions and sometimes even from regular banks.

As an owner/manager of an SME, therefore, it is important for you to look after the intellectual property of your SME not only as a legal asset but also as a financial instrument.

Using IP assets to finance your business

IP assets may help you to strengthen your case for obtaining business finance from investors/lenders. The investor/lender, be it a bank, a financial institution, a venture capitalist, or a business angel, in undertaking an appraisal of the request for equity assistance or loan, will assess whether the new or innovative product or service offered by the SME is protected by a patent, a utility model, a trademark, an industrial design, or copyright or related rights.

Such protection is often a good indicator of the potential of your SME for doing well in the marketplace. IP ownership is thus important to convince investors/lenders of the market opportunities open to the enterprise for the commercialisation of the product or service in question. On occasions, a single powerful patent may open doors to a number of financing opportunities.

Ownership of IP rights over the creative output or innovations related to the products or services that an enterprise intends to market, guarantees a certain degree of exclusivity and, thereby, a higher market share if the product/service proves successful among consumers.

Different investors/lenders may value your IP assets in different ways and may attach different degrees of importance to IP rights. A clear trend, however, is developing towards an increasing reliance on IP assets as a source of competitive advantage for firms. Thus investors/lenders are increasingly focusing on firms with a well-managed IP portfolio, even though they encounter, even in the developed countries, many new problems and issues while trying to perfect security interests in intellectual property.

As the owner/manager of an SME, you must therefore take steps to understand the commercial value of the IP assets of your SME, ensure their proper valuation by professionals if need be, and understand the requirement(s), if any, for their proper accounting in the accounts books and balance sheet.

Above all, make sure to include the IP assets of your SME in your business plan when presenting it to potential investors/lenders.

Securitisation of IP assets — a new trend

Lending partly or wholly against IP assets is a recent phenomenon even in developed countries. Collateralising commercial loans and bank financing by granting a security interest in IP is a growing practice, especially in the music business, Internet-based SMEs and in high technology sectors. Securitisation normally refers to the pooling of different financial assets and the issuance of new securities backed by those assets. In principle, these assets can be any claims that have reasonably predictable cash flows, or even future receivables that are exclusive. Thus securitisation is possible for future royalty payments from licensing a patent, trademark or trade secret, or from musical compositions or recording rights of a musician. In fact, one of the most famous securitisations of recent years involved the royalty payments of a rock musician in the USA, namely, Mr David Bowie.

At present, the markets for intellectual property asset-based securities are small, as the universe of buyers and sellers is limited. But if the recent proliferation of IP exchanges on the Internet is an indication, then it is only a matter of time before all concerned will develop greater interest and capacity to use IP assets for financing business start-ups and expansions. As more cash flows are generated by intellectual property, more opportunities will be created for securitisation.

Proper valuation of IP for obtaining finance

While securitisation appears to be gaining ground, conventional lending remains the main source of external finance for most SMEs. The practice of extending loans secured solely by IP assets is not very common in the developing world, Zimbabwe included. In fact, it is practiced more by venture capitalists than by banks. If you seek to use IP assets as collateral to obtain financing, your IP assets stand a greater chance of being accepted as collateral if you are able to prove their liquidity and that they can be valued separately from your business. Furthermore, you have to show that your IP assets are durable, at least for the period during, which you have to repay the loan, and marketable in the event of foreclosure or bankruptcy.

In this respect, it is critical to identify all the IP assets of your SME and to obtain an objective valuation of the identified assets from a competent valuation firm. The value of IP management processes, which identify, log, track and quantify your IP assets becomes increasingly important in the Internet economy. This is one more reason for you to increase in-house awareness of the extent and value of IP asset holdings, including trade secrets, which might be used to collateralise a loan.

It is true that until now the valuation of intellectual property is considered to be highly subjective by both lenders and borrowers. While well-founded valuation methodologies exist, they are either considered to be too subjective or are not generally understood by most people.

The increasing use of royalty streams arising from licensing to determine the value of intellectual property is a welcome development in enhancing the acceptability of intellectual property assets as valuable assets providing security for debt financing and equity participation.

As an SME, it is therefore important to keep this aspect in mind while seeking financial assistance in particular, and while developing your business strategy and business plan in general.

Aleck Ncube is an Intellectual Property Scholar based in Bulawayo. He can be contacted on aleckncube@gmail,com or followed on Twitter: @aleckncube

You Might Also Like

-

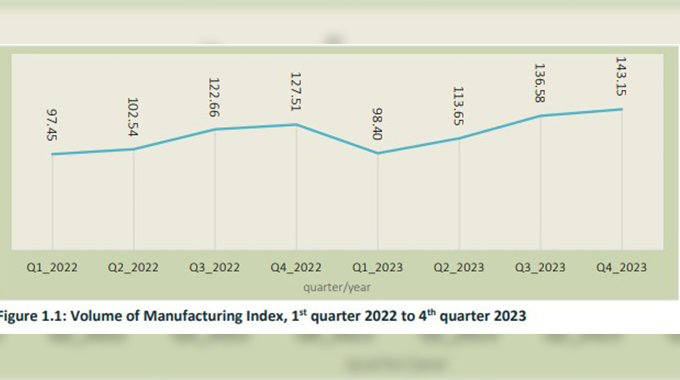

Sikhulekelani Moyo ZimStats says the manufacturing index for the 2023 fourth quarter registered a 12,26 year on year percentage increase to 143,15 when compared compared to 127,51 recorded in the prior year. Volume of the manufacturing index (VMI) is an economic indicator that shows relative changes in the volume of output in the manufacturing sector over time, […]

Agriculture Journal

Comments